After a storm rolls through, there’s a lot to deal with at once: shingles in the yard, water coming in somewhere, and no clear sense of what to do first. This checklist walks you through it in order, from safety to permanent repairs, with Michigan-specific guidance on insurance and contractor licensing.

Have a question about this topic?

Ask Roofster — our AI roofing expert is available 24/7.

Stay Safe and Assess From the Ground

Do not climb onto a storm-damaged roof. Compromised decking, loosened shingles, and hidden structural damage make it dangerous.

Check from the ground and inside your home:

• Downed power lines — if any wire is on the ground or touching your home, stay away and call 911.

• Gas smell — leave immediately and call your gas utility’s emergency line from outside.

• Structural shifts — sagging rooflines, cracked walls, or doors that suddenly won’t close. Call your local building department.

• Interior water — check ceilings, walls, and attic for active leaks. If water is near electrical fixtures, turn off the breaker for that circuit first.

Use binoculars from the yard to scan for missing shingles, dented flashing, or debris. That’s enough for now. The detailed inspection comes later.

Key takeaway: A damaged roof can wait an hour. A fall or electrocution cannot.

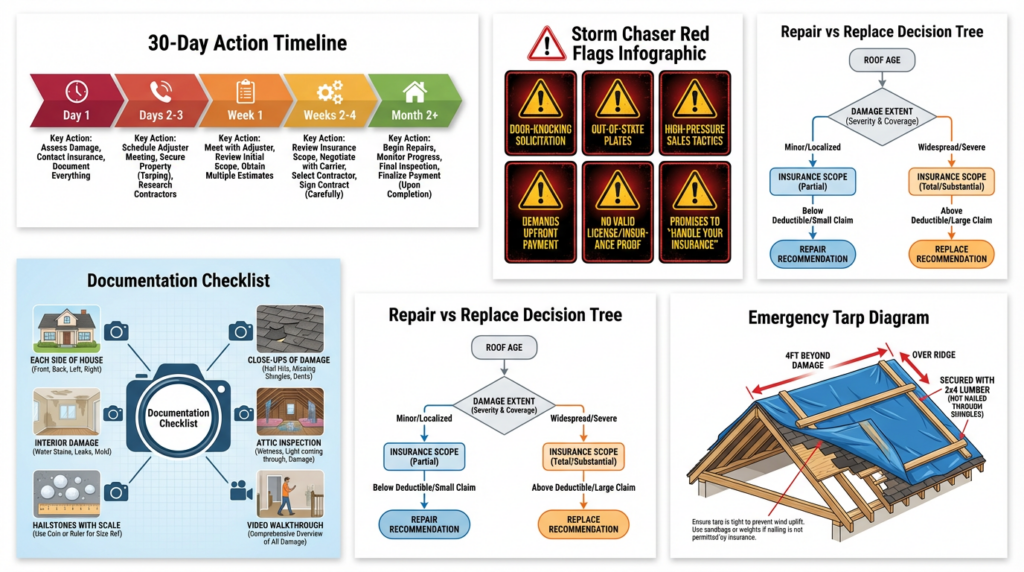

Document Everything Before You Touch Anything

Before you move debris, tarp anything, or clean up, grab your phone:

• Exterior: Photograph every issue — missing shingles, dented gutters, cracked siding, broken windows, fallen limbs. Shoot wide angles of each side of the house and close-ups of each damaged area.

• Interior: Water stains, wet drywall, warped flooring, damaged belongings. Date-stamp everything.

• Hailstones: Put several in a freezer bag next to a coin for scale. This evidence supports your claim if the adjuster arrives days later.

Shoot video walkthroughs too. Narrate what you see — the side of the house, the date, the specific damage. Save everything to cloud storage immediately.

Key takeaway: Your photos and video are the foundation of your insurance claim. Document first, clean up second.

Make Emergency Temporary Repairs

Michigan’s spring storms often come in clusters. Protect your home from further water intrusion before the next round of rain.

Tarping: Use a heavy-duty blue tarp (6-mil or thicker). Extend it at least 4 feet past the damaged area on all sides and secure it with 2×4 lumber and cap nails along the edges. Don’t nail through shingles to hold it down. If you can’t safely reach the damage, call a contractor for emergency tarping.

Inside: Move valuables away from active leaks. Place buckets under drips. If water is pooling behind a ceiling, poke a small drain hole in the center of the bulge to prevent collapse.

Save every receipt. Your homeowner’s insurance covers reasonable mitigation expenses — tarps, buckets, emergency materials, even hotel costs if the home is uninhabitable. You’ll submit these with your claim.

File Your Insurance Claim

Call your insurance company within 24-48 hours. Most Michigan homeowner’s policies require filing within 1 year of the loss date (some allow 2 years — check your declarations page).

On the call: provide your policy number, the storm date, and a general description of the damage. Don’t agree to a recorded statement on the first call. Don’t accept a settlement amount over the phone before a professional inspection.

The insurer will assign a claims adjuster to inspect your property, typically within 5-14 days. Write down your claim number and reference it in every future communication.

If your claim is denied or delayed, Michigan homeowners can file a complaint with the Department of Insurance and Financial Services (DIFS) at michigan.gov/difs or call 877-999-6442. For the full step-by-step process, see our guide to filing a roof insurance claim in Michigan. Our homeowner’s guide to insurance policies covers what your policy should include before the next storm.

Get a Professional Roof Inspection

A proper storm damage inspection goes beyond a quick walk-around. A licensed Michigan contractor should check shingles for hail bruising (circular dents that expose the mat beneath the granule layer), lifted or separated flashing around chimneys and vents, cracked vent boots, and the attic underside for daylight through decking or wet insulation.

You can verify any contractor’s license at Michigan LARA. A licensed local contractor carries Michigan-required insurance and will still be here next year if something goes wrong.

Get your contractor’s inspection report before the insurance adjuster visits. Having your own professional assessment means you’re not relying solely on the adjuster’s scope. Learn more about what happens during a roof inspection or the benefits of a free professional roof inspection.

Protect Yourself From Storm Chasers

Within 48 hours of a major storm, trucks with out-of-state plates start rolling through Michigan neighborhoods offering “free inspections.” Some are legitimate. Many are not.

Watch for these red flags: door-to-door solicitation right after the storm, no verifiable Michigan contractor license, pressure to sign immediately, demands for full payment upfront, and promises to “handle your insurance for you.” The risk is real — they collect the insurance payment, leave the state, and six months later their phone is disconnected and their warranty is worthless.

Before signing with anyone, verify their license at Michigan LARA, check Google reviews for local job site photos, and ask for proof of Michigan general liability and workers’ comp insurance. Our guide to choosing the right roofing contractor covers what to look for in more detail.

Repair or Replace

Michigan’s freeze-thaw cycles accelerate storm damage faster than moderate climates. A cracked shingle lets water in before the first freeze, where it expands inside the shingle mat and decking. By spring, one damaged shingle becomes a compromised section.

General guidelines:

• Repair if damage is isolated to one area, the roof is under 10 years old, and undamaged sections show no wear.

• Replace if damage spans multiple slopes, the roof is over 15 years old, or the inspection reveals pre-existing issues the storm worsened.

• Insurance may decide for you — if the adjuster’s scope covers more than 50% of the roof area, most carriers approve full replacement.

Your contractor should walk you through this with specifics. For cost expectations, see our breakdowns of roof repair costs and roof replacement costs in Michigan. If your roof needs a full replacement, our roofing materials buyer’s guide can help you compare options.

Your 30-Day Timeline

| When | What to do |

| Day 1 | Confirm safety. Document all damage. Tarp exposed areas. Save receipts. |

| Days 2-3 | File insurance claim. Contact a licensed local contractor for inspection. |

| Week 1 | Get contractor’s inspection report. Review your policy (ACV vs. RCV, deductible, deadlines). Don’t start permanent repairs before the adjuster inspects. |

| Weeks 2-4 | Attend adjuster’s inspection (have your contractor present). Review scope of loss. If the scope seems low, your contractor can file a supplement. Approve the repair plan. |

| Month 2+ | Complete permanent repairs. Collect depreciation holdback if applicable. File final documentation. If underpaid, file a DIFS complaint (877-999-6442). |

Frequently Asked Questions

Does homeowners insurance cover storm damage to a roof?

Standard Michigan homeowner’s policies (HO-3) cover sudden storm damage from wind, hail, fallen trees, and lightning. They typically don’t cover damage from lack of maintenance or gradual wear. Check your declarations page for exclusions and deductible amounts.

How long do I have to file a claim for roof damage in Michigan?

Most policies require filing within 1 year of the storm date, though some allow up to 2 years. Check your policy’s conditions section for the exact deadline. File as soon as possible — delays give insurers grounds to question the timeline.

How do I know if my roof has storm damage?

From the ground, look for missing or displaced shingles, dented gutters, cracked siding, and debris on the roof. Inside, check ceilings and attic for water stains, daylight through the decking, or wet insulation. Circular dents on metal vents and downspouts usually mean the roof has matching hail bruising. A professional inspection is the only way to confirm the full extent.

Should I repair or replace my roof after storm damage?

Isolated damage on a newer roof usually calls for repair. Widespread damage on a roof over 15 years old, or damage that reveals pre-existing deterioration, typically warrants replacement. Your contractor and insurance adjuster will both weigh in. Financing options are available if replacement costs are a concern.

Get a Free Storm Damage Inspection

If your roof took a hit in a recent storm, Weather Vane Roofing will inspect the damage and give you an honest assessment — no pressure, no obligation. We’ll walk you through the insurance process, handle the supplement paperwork if needed, and stand behind every repair with our lifetime workmanship guarantee.Schedule your free inspection or call us today.