After a storm, there are shingles in the yard and a wet spot on the ceiling. The roof insurance claim process is straightforward if you know the steps ahead of time.

Have a question about this topic?

Ask Roofster — our AI roofing expert is available 24/7.

When Should You File a Roof Insurance Claim?

Not every roof issue warrants a claim. Filing for cosmetic damage or normal wear can lead to a denial, and the claim still goes on your record.

Typically covered: hail, wind (including derechos), fallen trees, ice dam damage, fire, lightning, and heavy debris.

Generally NOT covered: normal aging, deferred maintenance, gradual leaks, and cosmetic-only damage.

If a specific weather event caused the damage, it is likely covered. If it built up over time, it probably is not. When you are unsure, a free roof inspection can tell you whether you are looking at storm damage or wear.

Key takeaway: File when a specific storm caused the damage.

Step 1: Document the Damage Before You Touch Anything

What you do in the first 24 hours matters most.

From the ground (do not climb on the roof), photograph missing shingles, dented gutters, broken siding, and downed limbs. Take wide shots and close-ups. Inside, photograph water stains and check the attic for daylight, wet insulation, or water trails on rafters.

Date-stamp everything. If there is hail, bag a few stones in the freezer next to a coin for scale.

Do not make permanent repairs yet. Tarp exposed areas, but do not replace shingles before the adjuster sees the roof. Save receipts for temporary materials since your policy covers mitigation costs. If you are dealing with missing shingles or exposed decking, temporary protection is critical while you wait.

Key takeaway: Date-stamped photos from the first 24 hours are your strongest evidence.

Step 2: Review Your Insurance Policy

Before you call your insurer, pull up your declarations page and check two things.

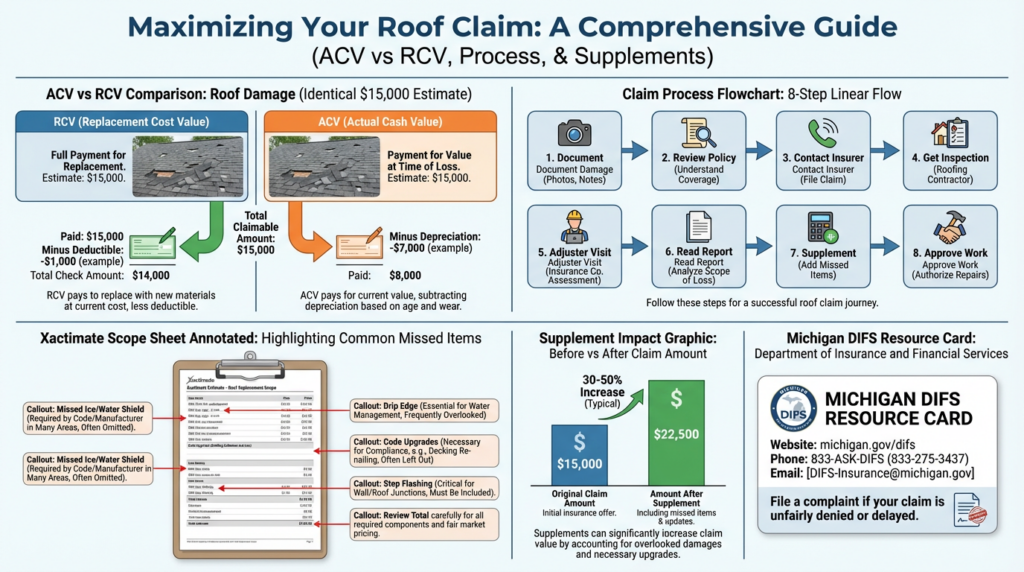

ACV vs. RCV. Replacement Cost Value (RCV) pays the full cost to replace your roof at today’s prices. Actual Cash Value (ACV) subtracts depreciation, so a 15-year-old roof could see a $15,000 job valued at only $8,000. Most Michigan HO-3 policies include RCV. With RCV, the insurer pays the depreciated amount first, then releases the “depreciation holdback” after repairs. You must finish the work to collect the full amount. Our homeowner’s guide to insurance policies covers these types in detail.

Your deductible. Common Michigan deductibles range from $1,000 to $2,500, though percentage-based deductibles (1-2% of insured value) can push that to $3,000 or more. If total damage is close to your deductible, filing may not be worth it.

Key takeaway: Know your coverage type and deductible amount before you file.

Step 3: Contact Your Insurance Company

Call your insurer’s claims line (not your agent’s office). Provide your policy number, the storm date, and a brief description. Ask for the claim number, adjuster contact info, and inspection timeline. Do not speculate about the cause or offer a repair estimate. In Michigan, you choose your own contractor.

Filing window: Most Michigan policies require filing within one year. File within weeks, not months.

Key takeaway: Call the claims line, get your claim number in writing, and file promptly.

Step 4: Get a Professional Roof Inspection

Before the adjuster arrives, get an independent assessment from a licensed Michigan roofing contractor. The adjuster assesses damage within the policy’s terms; your contractor advocates for you.

A thorough inspection covers every roof plane, checks for hail bruising and wind lift, examines flashing and vent boots, and includes an attic check. What happens during a roof inspection explains the full process. A reputable contractor provides this at no cost on insurance claims. Our storm damage checklist helps you track what to look for.

Key takeaway: Your contractor documents damage the adjuster may miss.

Step 5: The Adjuster Visit and Report Review

Have your contractor present when the adjuster inspects. The adjuster documents damage, measures the roof, and creates a line-by-line “scope of loss” in Xactimate software (a detailed repair estimate). Your contractor ensures code-required items are included, like ice and water shield in valleys and at eaves.

Within days to two weeks, you receive the Xactimate estimate. Do not just check the bottom-line number. Verify line items cover tear-off, shingles, underlayment, flashing, ridge cap, drip edge, ice and water shield, pipe boots, ventilation, and labor. Confirm quantities match your roof’s actual measurements (1 “square” = 100 sq ft). Our guide to roof repair costs in Michigan covers what these items typically cost.

Key takeaway: Read the line items, not just the total. Missing code items can mean thousands left off your claim.

Step 6: Supplements and Choosing Your Contractor

A supplement is a formal request to add items or adjust quantities on the original scope. They are routine. Once tear-off begins, contractors often find hidden decking or underlayment damage. Your contractor documents the gap, submits photos and code references, and the adjuster issues additional payment. On a typical Michigan replacement, supplements recover 30-50% beyond the original payment. Our roof replacement cost guide walks through the numbers for Mid-Michigan homes.

When choosing a contractor, verify their license through Michigan LARA at michigan.gov/lara. Red flags: door-knocking right after the storm, out-of-state plates, pressure to sign before the claim is processed, or offering to “cover your deductible” (insurance fraud in Michigan). Our guide to choosing the right roofing contractor covers the full vetting process.

Key takeaway: Supplements recover significant additional value. Choose a licensed local contractor.

What If Your Claim Is Denied?

A denial is not the end. You can request a re-inspection, invoke the appraisal clause (both sides hire independent appraisers who select an umpire), or file a complaint with Michigan DIFS at michigan.gov/difs (833-ASK-DIFS).

Key takeaway: Re-inspections, the appraisal clause, and DIFS protect homeowners after a denial.

Avoid These Costly Mistakes

• Waiting too long to file. Storm damage gets harder to prove as it weathers.

• Repairing before the adjuster visits. Tarping is fine. Replacing shingles means the adjuster cannot verify the damage.

• Accepting the first estimate without review. Have your contractor check for missed items.

Preparing your roof before storm season also reduces the chance of severe damage.

Frequently Asked Questions

How long do I have to file in Michigan?

Most policies require filing within one year. Filing within the first few weeks is stronger because damage is fresher and easier to document.

Should my roofer be present when the adjuster comes?

Yes. Your contractor spots missed damage, ensures code requirements are included, and creates documentation that supports supplements.

What is the supplement process?

A supplement adds items or adjusts quantities on the original scope. They typically recover 30-50% additional claim value.

We Walk You Through Every Step

Weather Vane Roofing has helped Mid-Michigan homeowners navigate hundreds of roof insurance claims. We provide free storm damage inspections, attend adjuster visits, review scope sheets, and handle supplements from start to finish.Schedule your free storm damage inspection and find out what your roof needs and what your policy covers.